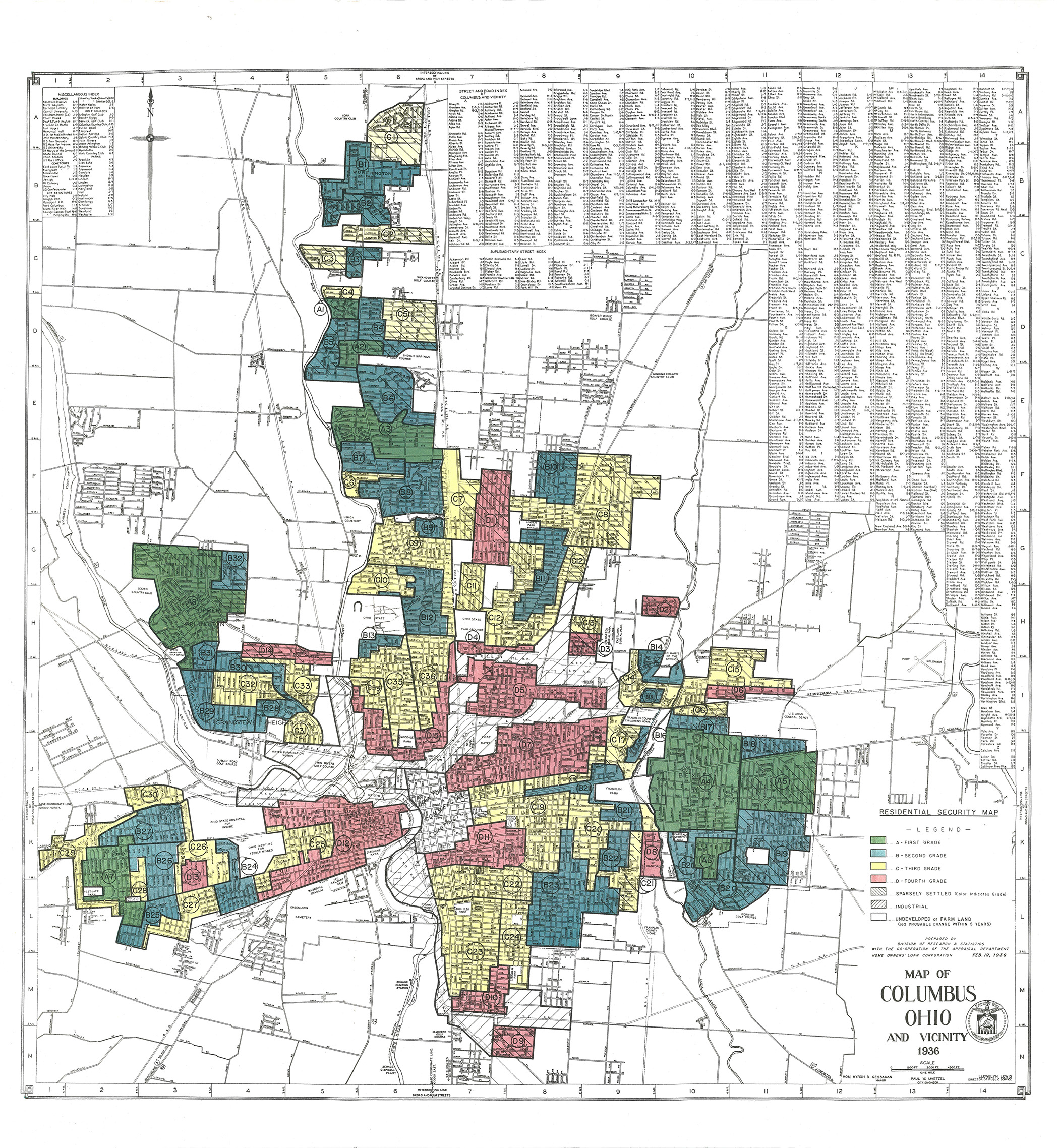

“The Home Owners’ Loan Corporation (HOLC) was created in June 1933 by the US Congress. The purpose was to refinance mortgages in default to prevent foreclosures. In 1935 Federal Home Loan Bank Board asked HOLC to look at 239 cities and create “residential security maps” indicating the level of security for real estate investments. On the maps, the newest areas — those considered desirable for lending purposes — were outlined in blue and known as Type A. These were typically affluent suburbs on the outskirts of cities. Type B neighborhoods were considered ‘Still Desirable,’ whereas older Type C neighborhoods were labeled ‘Declining’ and outlined in yellow. Type D neighborhoods were outlined in red and were considered the most risky for mortgage support.” The outcome of the practice of “redlining” was to deny mortgages and business loans to minorities and lower income borrowers.

The original Columbus “Redlining” map from 1936 is below, followed by an interactive version. A 12.2mb jpg file of the map is here.

Source: Federal Home Owners’ Loan Corporation (HOLC) Maps (“Redlining Maps”) for Ohio Cities (Ohio State University Libraries)

Interactive Columbus “Redlining” map from 1936:

The link to the digitized maps appears broken. I think they’re here now: http://guides.osu.edu/maps-geospatial-data/maps/redlining

Thanks for the new URL. Fixed on the page. John K.

A lot of the high risk mortgage is in places I thought it would never be in

Redlining is complicated. The Kirwan Institute at OSU has done a lot of work on this issue: http://kirwaninstitute.osu.edu

In 2020, REDLINING still exists in Columbus neighborhoods. One of my friends, along with my assistance, attempted to refinance his home, but his own bank, not only denied him a refinance, but would not even call him to tell him that he was denied refinancing due to REDLINING by his own bank.

I would be interested in knowing when/how “redlining” crossed into racial discrimination vs poverty (or riskier loans) evaluation.

I’m assuming “intent” was risk, not race.

Yet, I also assume that once released this tool became utilized by those with a different agenda.

Anyone have specifics (not necessarily Columbus based).

Trying to better sort out the facts from intended or unintended consequences.

Thank you,

OSU’s Kirwan Institute has done quite a bit of work on this, and they are worth contacting:

http://kirwaninstitute.osu.edu

I’m actually in Orlando Florida. This Orlando map actually says it’s the negro zone. Not very subtle. https://bungalower.com/2017/10/25/redlining-still-affects-orlandos-neighborhoods/

Read this, it all started before 1933.

It was a process that took months, and years. Also imagine you lived in a redlined neighborhood, and you were asking for a loan to move into a better neighborhood, do you think that the federal bank would give you a loan after you provided your zip code, a redlined area?

https://fcvoters.org/2020/02/26/not-in-my-backyard-systematic-racism-and-redlining/